Crypto Beginner Series EP 3: What is Blockchain?

Believe it or not, we’re up to the third episode in this blockchain beginner series and we are only now getting to what a blockchain is. This industry is incredibly complex, but also provides an incredible opportunity to those who take the time to understand it.

In the first two articles, we look at what is Bitcoin and then take a more general overlook of what cryptocurrencies are. But now it is time to start looking into the tech underlying this new and burgeoning industry.

Blockchain is not Bitcoin

I couldn’t tell you the number of times I’ve told people I work in the blockchain industry and they don’t understand. Then I say “Bitcoin” and they all of a sudden seem to comprehend what I’m talking about. In reality, that’s like me saying I work in the electronic industry and no one understanding until I say “computers”.

Before I go into how this software works, I need to explain what is the information that blockchains record. They record transactions. By transactions, I don’t mean financial transactions, although in the form of a cryptocurrency, this is the case. What I mean are data transactions, the sending, receiving, or changing of data. Remember a blockchain is a digital ledger, and a ledger doesn’t just store numbers, it could be a list of items, a store’s product range, a person’s history, ownership certificates, or just about anything that can be recorded.

Ok, so you know that a blockchain is a type of software program and that it stores transactions of data. The way it works is that it takes these pieces of data and assigns a string of characters, to them by hashing them — you could think of it as similar to encrypting the data.

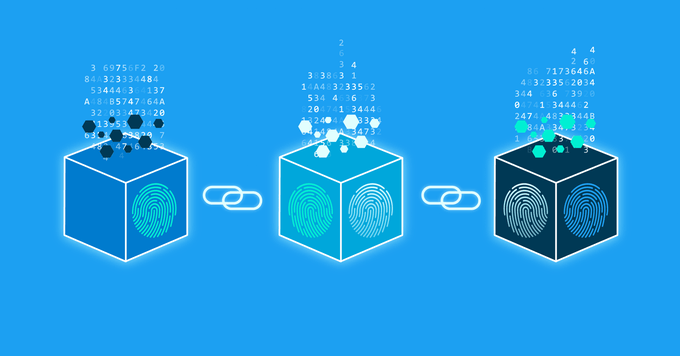

Block + Block = Blockchain

Now, this string of characters is similar to an ID and is called that transaction’s hash. Once a number of these hashes have been created, they get arranged into a “digital page,” called a block. As soon as the block is full, it gets checked for accuracy, and once confirmed, it is recorded onto the ledger.

While this checking is going ahead, the next block starts to receive hashes. Once it is full, it gets checked and then added to the ledger, immediately after the last block. As this process continues, a chain of blocks is formed, and you get the blockchain.

Included in each block is an identifier linking it to the previous block and one which will be used by the next block to link to it. Think of this like the connectors used by trains to hook up a series of carriages together.

Accessing the data

Now anyone who has access to the blockchain has access to the blocks. But all that is inside these blocks are hashes, hundreds and hundreds of random strings of characters. This is one of the genius parts of blockchain technology. These hashes can be used to verify information, but not extract information.

What I mean by this is that if you want to confirm if something is true, like does a particular location hold enough stock, or is this particular wallet the owner of an item. But what you can’t do, is take a hash and extract all the information out of it without permission. This ensures privacy while allowing the ledger to be useful still.

Now sometimes a user might need more specific information from the blockchain, and if they meet the criteria, or hold the correct key, they can unlock that specific piece of information. This is more so for permissioned blockchains, but I’ll get to this later in this article.

So why decentralized?

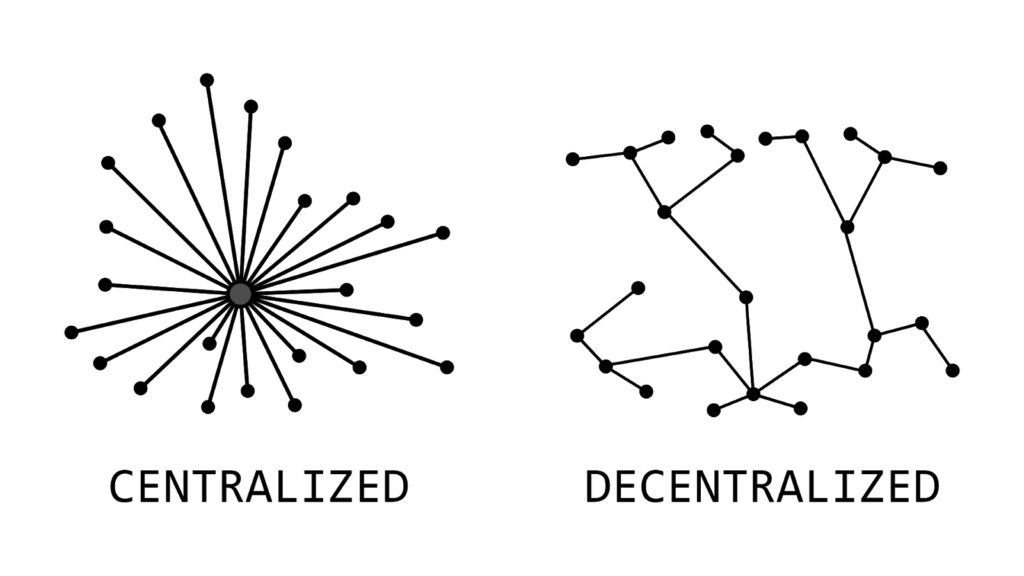

Now let me quickly explain what decentralized means. Software needs to be saved somewhere. It needs a hard drive to be stored on and run from. Traditionally, online programs are stored on servers from the organization in charge of the software. Other software is stored locally on the end user’s device. In other words, there is a central server or device which is used to run or control the program.

Decentralization means the opposite of this, that is, there is no one device or central server which runs the program or controls it. This is critical when the different parties accessing or interacting with the software do not trust each other. It’s all about security and trust.

Now you know how I mentioned that not all blockchains are decentralized? There’s a good reason for that. A blockchain should only be decentralized if it is required. A company that is using blockchain as a means to accurately store its data in an automated manner on its own servers has no trust issues as it is the only party interacting with the data. Thus spreading the blockchain over multiple servers at different locations has little value for the cost involved.

Trust issues

But a public piece of software, with multiple users who complete actions on it, has massive trust issues. How do we know the data is recorded on the blockchain accurately, and how do we know it wasn’t manipulated? The answer is decentralization.

When a blockchain is decentralized, the ledger is stored on many devices all around the world. These devices connected to the network are called nodes. When a block is filled, it must get confirmed by all the other nodes on the network, or at least enough to guarantee accuracy. This means to create false information on the ledger, you would need to access each ledger on every node and change it simultaneously to let the block with the fake information be confirmed and added to the chain. No one knows who the other nodes are or where they are located. The complexity and difficulty in achieving this “takeover” are so incredible that it simply isn’t worth it for the reward.

For some blockchains, there is another way to add fake information, and that is through a 51% attack. This is where you control or own at least 51% of the nodes on the network in order to make the changes through “majority rules.” Again, unless the network is extremely small, this is very costly and difficult to do.

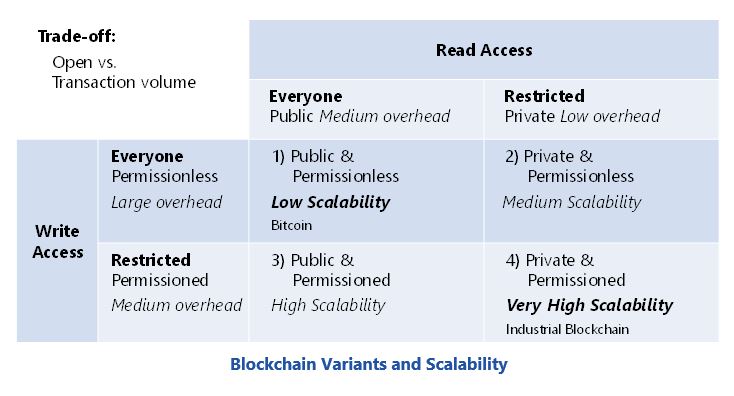

Public vs. Private

Another aspect that varies among blockchains is if they are public or private, also whether they are permissioned or permissionless. Basically, what it means is can anyone use it (permissionless) or access it (public), or can it only be used (permissioned) or accessed (private) by those who have been invited or hold a key. Think of Google, and all the data it collects from everyone who uses it. How many people trust the company to not share their data? How many people have the ability to do something about it?

Now imagine all this data stored on a public blockchain. Remember the specific data is hidden behind the hashes, and the only way to access it is by putting in a call requesting the information. This means that everyone will be able to see every time Google tries to access this information. The transparency that this provides is incredibly powerful.

This trust and transparency are what make Bitcoin and the other cryptocurrencies so powerful. They create a financial system with no governing body.

Even though Bitcoin is the most famous blockchain, it is only one example of blockchain’s potential. There is a myriad of uses for this technology in a range of industries, including travel, governance, commerce, automotive, tracing, real estate, art, collectibles, gaming, education, agriculture, shipping, and legal. In fact, almost every industry can benefit in some manner from blockchain technology.

If you’d like to get into cryptocurrencies, let me walk you through how to set up your first crypto wallet.

Written by Joshua Mapperson.